A Comprehensive Guide to Understanding ABARouting Code: Everything You Need to Know

ABA Routing Code plays a pivotal role in the financial ecosystem, ensuring seamless transactions and secure fund transfers. It is a nine-digit code that serves as the backbone of banking operations in the United States. Understanding its importance and functionality is crucial for both individuals and businesses alike. Whether you're making a direct deposit, setting up automated payments, or wiring money, knowing your ABA Routing Code is essential.

As financial systems continue to evolve, the ABA Routing Code remains a fundamental component of modern banking. This code helps banks identify each other and streamline the process of transferring funds. Without it, transactions would be significantly slower and more prone to errors. This article aims to provide a detailed and comprehensive overview of ABA Routing Codes, ensuring you have the knowledge to navigate financial processes with confidence.

In today's digital age, where financial transactions occur at lightning speed, the importance of ABA Routing Codes cannot be overstated. From small businesses to large corporations, everyone relies on these codes to ensure smooth and secure financial operations. By understanding how they work and their significance, you can better manage your finances and avoid potential pitfalls.

What is ABA Routing Code?

The ABA Routing Code, also known as the Routing Transit Number (RTN), is a nine-digit code assigned to financial institutions in the United States. Its primary purpose is to facilitate the identification of banks during financial transactions. This code ensures that funds are directed to the correct institution, reducing the risk of errors and delays.

Each bank or credit union in the U.S. has its own unique ABA Routing Code. This code is used in various financial activities, including direct deposits, electronic funds transfers (EFTs), and check processing. Understanding how this code works can help you manage your finances more effectively and avoid potential issues during transactions.

Why is ABA Routing Code Important?

- Facilitates secure and accurate fund transfers

- Helps identify specific financial institutions

- Reduces the risk of errors in financial transactions

- Supports the automation of banking processes

History of ABA Routing Code

The ABA Routing Code was first introduced in 1910 by the American Bankers Association (ABA) to standardize the process of check clearing. Before this, the system was fragmented, leading to inefficiencies and errors. The introduction of the Routing Code revolutionized the banking industry, making it easier to process checks and transfer funds.

Over the years, the ABA Routing Code has evolved to accommodate advancements in technology and the increasing complexity of financial transactions. Today, it remains a crucial component of the U.S. banking system, supporting both traditional and digital banking operations.

Key Milestones in the Development of ABA Routing Code

- 1910: Introduction of the ABA Routing Code

- 1950s: Adoption of magnetic ink character recognition (MICR) technology

- 1970s: Integration with electronic funds transfer systems

- 2000s: Expansion to support online banking and mobile transactions

Structure of ABA Routing Code

An ABA Routing Code consists of nine digits and follows a specific format. The first four digits represent the Federal Reserve Routing Symbol, which identifies the Federal Reserve Bank responsible for processing transactions. The next four digits are the ABA Institution Identifier, which uniquely identifies the financial institution. The final digit is a check digit, used to validate the accuracy of the code.

This structured format ensures that each ABA Routing Code is unique and can be easily verified. By understanding the components of the code, you can better appreciate its role in maintaining the integrity of financial transactions.

Breaking Down the ABA Routing Code

- First four digits: Federal Reserve Routing Symbol

- Next four digits: ABA Institution Identifier

- Last digit: Check digit

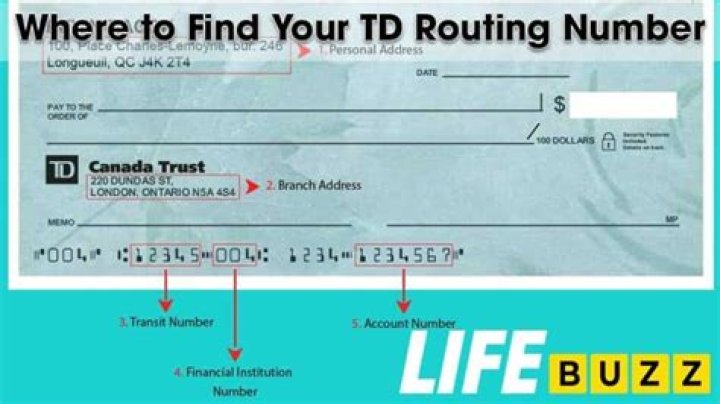

How to Find Your ABA Routing Code

Locating your ABA Routing Code is a straightforward process. The most common method is to check your checks, where the code is printed at the bottom left. Alternatively, you can find it on your bank statements or by logging into your online banking account. Many banks also provide this information on their websites or through customer service.

When searching for your ABA Routing Code, ensure that you are using the correct code for the specific type of transaction you are conducting. Some banks may have different codes for domestic and international transactions, so it's essential to verify the appropriate code before proceeding.

Methods to Find Your ABA Routing Code

- Check the bottom of your checks

- Review your bank statements

- Log in to your online banking account

- Visit your bank's website

- Contact customer service

Uses of ABA Routing Code

The ABA Routing Code is utilized in various financial transactions, ensuring that funds are transferred accurately and efficiently. Some of the most common uses include:

- Direct deposits: Used to deposit salaries, pensions, and government benefits directly into your account

- Electronic funds transfers (EFTs): Facilitates the transfer of funds between accounts

- Check processing: Ensures checks are cleared and funds are credited to the correct account

- Automated Clearing House (ACH) transactions: Supports recurring payments, such as utility bills and loan repayments

By understanding the different applications of ABA Routing Codes, you can better manage your financial transactions and avoid potential issues.

ABA vs. SWIFT Code

While ABA Routing Codes are primarily used for domestic transactions within the United States, SWIFT Codes are employed for international transactions. A SWIFT Code, also known as a Bank Identifier Code (BIC), is an alphanumeric code that identifies banks globally. Unlike ABA Routing Codes, SWIFT Codes consist of eight to eleven characters and provide additional information about the specific branch of the bank.

Understanding the differences between ABA Routing Codes and SWIFT Codes is crucial when conducting international transactions. Using the correct code ensures that your funds are transferred securely and efficiently.

Key Differences Between ABA Routing Codes and SWIFT Codes

- ABA Routing Codes: Used for domestic transactions in the U.S.

- SWIFT Codes: Used for international transactions

- ABA Routing Codes: Nine-digit numeric code

- SWIFT Codes: Eight to eleven-character alphanumeric code

Common Mistakes to Avoid

Mistakes involving ABA Routing Codes can lead to delays, errors, or even the rejection of transactions. Some common mistakes include:

- Using the wrong code for the type of transaction

- Entering the code incorrectly

- Not verifying the code before initiating a transaction

To avoid these issues, always double-check the ABA Routing Code before proceeding with any financial transaction. If you're unsure, consult your bank or financial institution for clarification.

Security and Privacy

While ABA Routing Codes are essential for financial transactions, it's important to protect this information to safeguard your accounts. Sharing your ABA Routing Code with unauthorized individuals can lead to unauthorized access and potential fraud. Always ensure that you only provide this information to trusted entities and secure platforms.

Additionally, many banks employ advanced security measures, such as encryption and multi-factor authentication, to protect your ABA Routing Code and other sensitive information. Staying informed about these security features can help you maintain the privacy and integrity of your financial data.

Frequently Asked Questions

Q: Can I use my ABA Routing Code for international transactions?

No, ABA Routing Codes are primarily used for domestic transactions within the United States. For international transactions, you will need to use a SWIFT Code.

Q: Is my ABA Routing Code the same as my account number?

No, your ABA Routing Code and account number are two separate pieces of information. The ABA Routing Code identifies your bank, while your account number identifies your specific account within that bank.

Q: How do I know if I'm using the correct ABA Routing Code?

To ensure you're using the correct ABA Routing Code, verify it by checking your checks, bank statements, or online banking account. If you're unsure, contact your bank or financial institution for confirmation.

Conclusion

The ABA Routing Code is a vital component of the U.S. banking system, ensuring secure and efficient financial transactions. By understanding its structure, uses, and importance, you can better manage your finances and avoid potential issues. Always verify your ABA Routing Code before initiating any transaction and take steps to protect this information to safeguard your accounts.

We encourage you to share this article with others who may benefit from this knowledge. If you have any questions or feedback, feel free to leave a comment below. For more informative content on personal finance and banking, explore our other articles on the website.