ABA Number Example: A Comprehensive Guide to Understanding and Using ABA Routing Numbers

ABA numbers, also known as routing transit numbers (RTNs), play a crucial role in facilitating seamless financial transactions across the United States. These nine-digit codes are essential for identifying financial institutions and ensuring that funds are transferred accurately and efficiently. Whether you're setting up direct deposits, paying bills online, or wiring money, understanding ABA numbers is vital for managing your finances effectively.

In today's digital age, where financial transactions occur at lightning speed, ABA numbers have become indispensable. They ensure that money moves between accounts without errors, saving both time and resources. As we delve deeper into this guide, we will explore the intricacies of ABA numbers, their structure, and how they function in various financial processes.

This article aims to provide a comprehensive overview of ABA number examples, helping you understand their significance and practical applications. By the end of this guide, you'll have a clear understanding of how ABA numbers work, their importance in the banking system, and how to use them effectively in your financial activities.

What is an ABA Number?

An ABA number, or American Banking Association number, is a unique nine-digit code assigned to financial institutions in the United States. This number serves as an identifier for banks and credit unions, ensuring that funds are routed correctly during transactions. ABA numbers were first introduced in 1910 by the American Banking Association to streamline the check-clearing process.

Today, ABA numbers are used for a wide range of financial activities, including direct deposits, automatic payments, and wire transfers. They are critical for both individuals and businesses, as they ensure that money is transferred accurately and securely.

Why Are ABA Numbers Important?

ABA numbers are important because they provide a standardized system for identifying financial institutions. Without them, the banking system would be prone to errors and inefficiencies. Here are some key reasons why ABA numbers are crucial:

- Facilitates accurate fund transfers

- Reduces the risk of transaction errors

- Supports automated banking processes

- Enhances the security of financial transactions

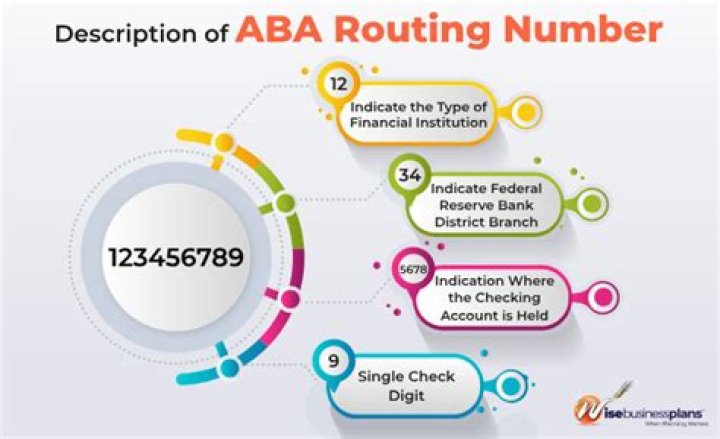

ABA Number Structure

The structure of an ABA number is carefully designed to ensure its functionality and uniqueness. Each digit in the nine-digit code carries specific information about the financial institution. Here's a breakdown of the ABA number structure:

Breaking Down the ABA Number

The first four digits of the ABA number represent the Federal Reserve routing symbol. These digits indicate the Federal Reserve Bank responsible for processing transactions for the financial institution. The next four digits are the ABA institution identifier, which uniquely identifies the bank or credit union. The final digit is a checksum digit, used to verify the validity of the ABA number.

For example, an ABA number like 123456789 can be broken down as follows:

- 1234: Federal Reserve routing symbol

- 5678: ABA institution identifier

- 9: Checksum digit

ABA Number Example

Let's take a look at a real-world example of an ABA number. Consider the ABA number 021000021, which belongs to JPMorgan Chase Bank. This number can be used for various financial transactions, such as setting up direct deposits or initiating wire transfers.

Here's how you might use this ABA number:

- When setting up direct deposit with your employer, you would provide this ABA number along with your account number.

- For wire transfers, you would include this ABA number in the transfer instructions to ensure the funds reach the correct bank.

How to Find Your ABA Number

Finding your ABA number is a straightforward process. Here are some common methods to locate your ABA number:

1. Check Your Paper Check

One of the easiest ways to find your ABA number is by looking at the bottom of your paper check. The ABA number is usually the first set of numbers printed in the magnetic ink character recognition (MICR) line.

2. Online Banking

Most banks and credit unions provide your ABA number through their online banking platforms. Simply log in to your account and navigate to the account details section to find your ABA number.

3. Contact Your Bank

If you're unable to locate your ABA number through the above methods, you can always contact your bank's customer service department. They will be happy to assist you in finding the correct ABA number for your account.

Uses of ABA Numbers

ABA numbers are used for a variety of financial transactions. Here are some of the most common uses:

1. Direct Deposits

Direct deposits allow employers to transfer salaries directly into employees' bank accounts. To set up direct deposit, you need to provide your ABA number and account number to your employer.

2. Automatic Payments

Automatic payments, such as bill payments and loan repayments, rely on ABA numbers to ensure that funds are transferred correctly. By providing your ABA number, you can automate recurring payments and avoid late fees.

3. Wire Transfers

Wire transfers are a fast and secure way to send money domestically or internationally. To initiate a wire transfer, you need to provide the recipient's bank ABA number along with other necessary details.

ABA vs ACH Number: What's the Difference?

While ABA numbers and ACH numbers are often used interchangeably, they serve slightly different purposes. An ABA number is used to identify a specific financial institution, while an ACH number is used specifically for electronic transactions processed through the Automated Clearing House (ACH) network.

In most cases, the ABA number and ACH number for a bank are the same. However, some banks may have different ACH numbers for domestic and international transactions. It's important to verify which number to use based on the type of transaction you're initiating.

Common Questions About ABA Numbers

Here are some frequently asked questions about ABA numbers:

1. Can I Use My ABA Number for International Transactions?

ABA numbers are primarily used for domestic transactions within the United States. For international transactions, you may need to use a SWIFT code instead of an ABA number.

2. Is My ABA Number the Same as My Account Number?

No, your ABA number and account number are not the same. The ABA number identifies your bank, while the account number identifies your specific account within that bank.

3. Can I Share My ABA Number?

Yes, you can share your ABA number with trusted parties for legitimate financial transactions. However, it's important to keep your account number confidential to protect your financial information.

History of ABA Numbers

The concept of ABA numbers dates back to 1910 when the American Banking Association introduced them to standardize the check-clearing process. Initially, ABA numbers were used primarily for check processing. Over time, their use expanded to include electronic transactions, wire transfers, and other financial activities.

Today, ABA numbers are an integral part of the U.S. banking system, facilitating billions of transactions annually. Their evolution reflects the growing complexity and sophistication of financial transactions in the modern era.

Importance of ABA Numbers in Banking

ABA numbers are essential for maintaining the integrity and efficiency of the banking system. They ensure that funds are transferred accurately and securely, reducing the risk of errors and fraud. By providing a standardized system for identifying financial institutions, ABA numbers play a critical role in supporting the smooth operation of the banking industry.

For individuals and businesses, ABA numbers offer convenience and peace of mind. They enable seamless financial transactions, saving time and resources. Whether you're setting up direct deposits, paying bills online, or wiring money, ABA numbers ensure that your transactions are handled efficiently and securely.

Security and Privacy Concerns with ABA Numbers

While ABA numbers are generally safe to share for legitimate financial transactions, it's important to exercise caution when disclosing your financial information. Protecting your ABA number and account number is crucial to safeguarding your financial privacy.

Here are some tips for ensuring the security of your ABA number:

- Only share your ABA number with trusted parties for legitimate transactions.

- Keep your account number confidential and avoid sharing it unnecessarily.

- Monitor your bank statements regularly for any unauthorized transactions.

- Enable two-factor authentication for your online banking accounts.

Conclusion

In conclusion, ABA numbers are a vital component of the U.S. banking system, facilitating accurate and secure financial transactions. By understanding their structure, uses, and importance, you can make the most of your banking experience. Whether you're setting up direct deposits, paying bills online, or wiring money, ABA numbers ensure that your transactions are handled efficiently and securely.

We encourage you to take action by reviewing your ABA number and ensuring that it is up-to-date for all your financial activities. If you have any questions or need further clarification, feel free to leave a comment below. Additionally, we invite you to explore our other articles for more insights into personal finance and banking. Together, let's build a more informed and financially secure future!

Data Sources: Federal Reserve, American Banking Association, Internal Revenue Service.