Federal Reserve ABA Numbers: A Comprehensive Guide to Understanding and Utilizing Them

Understanding Federal Reserve ABA numbers is essential for anyone dealing with banking transactions in the United States. These numbers play a crucial role in ensuring that funds are transferred accurately and efficiently between financial institutions. By familiarizing yourself with how ABA routing numbers work, you can streamline your banking processes and avoid potential errors.

When you initiate a wire transfer, direct deposit, or any other electronic transaction, the Federal Reserve ABA number acts as a digital address that directs the money to the correct bank. This guide will walk you through everything you need to know about these numbers, from their structure and purpose to how to locate them and use them effectively.

Whether you're an individual managing personal finances or a business handling large-scale transactions, understanding Federal Reserve ABA numbers can save you time, money, and headaches. Let's dive into the details to ensure you're well-equipped to navigate the world of banking transactions.

What Are ABA Numbers?

ABA numbers, also known as routing transit numbers (RTNs), are nine-digit codes assigned to financial institutions in the United States. These numbers serve as identifiers for banks and credit unions, ensuring that transactions are routed to the correct institution. The American Bankers Association (ABA) introduced these numbers in 1910 to standardize banking operations.

The Federal Reserve plays a pivotal role in managing and regulating ABA numbers. Each number is unique to a specific financial institution and location, making it easier to track and verify transactions. By understanding how ABA numbers work, you can ensure that your financial transactions are processed accurately and efficiently.

Importance of Federal Reserve ABA Numbers

Federal Reserve ABA numbers are critical for several reasons:

- They ensure accurate routing of funds between banks.

- They help prevent fraud by verifying the legitimacy of transactions.

- They streamline the process of electronic payments and transfers.

History of ABA Numbers

The history of ABA numbers dates back to 1910 when the American Bankers Association sought to create a standardized system for routing checks and other financial instruments. Initially, ABA numbers were designed to simplify the check-clearing process, but their utility has expanded significantly over the years.

As electronic banking became more prevalent, the role of ABA numbers evolved to include wire transfers, direct deposits, and automated clearing house (ACH) transactions. The Federal Reserve's involvement in regulating and maintaining these numbers ensures their continued relevance in modern banking systems.

Evolution of Federal Reserve ABA Numbers

Over the decades, Federal Reserve ABA numbers have undergone several changes to adapt to new technologies and banking practices:

- Expansion of ACH transactions.

- Integration with international banking systems.

- Enhanced security measures to combat fraud.

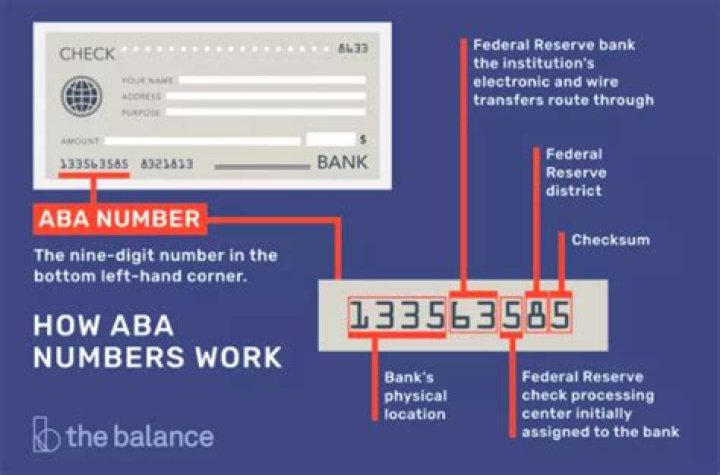

Structure of ABA Numbers

Each ABA number consists of nine digits, each serving a specific purpose:

- First four digits: Identify the Federal Reserve routing symbol.

- Next four digits: Represent the bank or financial institution's identifier.

- Last digit: Acts as a check digit to verify the accuracy of the number.

Understanding the structure of Federal Reserve ABA numbers is essential for ensuring that transactions are processed correctly. Banks and financial institutions rely on these numbers to route funds efficiently and securely.

Federal Reserve and ABA Numbers

The Federal Reserve plays a crucial role in managing and regulating ABA numbers. As the central banking system of the United States, the Federal Reserve ensures that these numbers are assigned and maintained according to strict standards.

Financial institutions must adhere to Federal Reserve guidelines when using ABA numbers for transactions. This includes verifying the accuracy of the numbers and ensuring they are up-to-date. By working closely with the Federal Reserve, banks can maintain the integrity of their ABA numbers and protect against fraud.

Regulatory Role of the Federal Reserve

The Federal Reserve's regulatory role in managing ABA numbers includes:

- Assigning and maintaining unique ABA numbers for financial institutions.

- Monitoring the use of ABA numbers to prevent misuse or fraud.

- Providing guidance and support to banks and credit unions.

Finding Your ABA Number

Locating your Federal Reserve ABA number is a straightforward process. You can find it in several places, including:

- On your checks: The ABA number is typically printed at the bottom-left corner of your checks.

- Online banking: Most banks provide ABA numbers through their online banking portals.

- Customer service: You can contact your bank's customer service department for assistance.

When searching for your Federal Reserve ABA number, ensure that you are using the correct number for the type of transaction you are conducting. Some banks may have different ABA numbers for wire transfers and ACH transactions.

Using ABA Numbers for Transactions

Federal Reserve ABA numbers are essential for a variety of transactions, including:

- Wire transfers: Use the ABA number to ensure funds are sent to the correct bank.

- Direct deposits: Provide your employer with the ABA number to set up automatic deposits.

- ACH transactions: Use the ABA number for electronic payments and bill payments.

When using Federal Reserve ABA numbers for transactions, double-check the number for accuracy to avoid processing delays or errors.

Tips for Using ABA Numbers

To ensure successful transactions, follow these tips:

- Verify the ABA number with your bank before initiating a transaction.

- Use the correct ABA number for the type of transaction you are conducting.

- Keep your ABA number secure and avoid sharing it unnecessarily.

Common Questions About ABA Numbers

Here are some frequently asked questions about Federal Reserve ABA numbers:

- What is the difference between an ABA number and a SWIFT code? ABA numbers are used for domestic transactions, while SWIFT codes are used for international transactions.

- Can I use the same ABA number for all types of transactions? It depends on your bank; some banks have different ABA numbers for wire transfers and ACH transactions.

- How do I find my ABA number if I don't have checks? You can find your ABA number through your bank's online portal or by contacting customer service.

ABA Number Security

Securing your Federal Reserve ABA number is crucial to protecting your financial information. Avoid sharing your ABA number unnecessarily and ensure that any transactions involving the number are conducted through secure channels.

Financial institutions employ various security measures to protect ABA numbers, including encryption and fraud detection systems. By staying informed about best practices for ABA number security, you can help safeguard your financial transactions.

Best Practices for ABA Number Security

To enhance the security of your Federal Reserve ABA number, follow these best practices:

- Never share your ABA number with unverified sources.

- Use secure channels for transactions involving ABA numbers.

- Monitor your accounts regularly for unauthorized transactions.

Future of ABA Numbers

As technology continues to evolve, the role of Federal Reserve ABA numbers may change to accommodate new banking practices and systems. Advances in digital banking, blockchain technology, and artificial intelligence could lead to new methods of routing and verifying transactions.

Despite these advancements, ABA numbers are likely to remain a key component of the U.S. banking system for the foreseeable future. By staying informed about developments in banking technology, you can ensure that your financial transactions remain secure and efficient.

Conclusion

Federal Reserve ABA numbers play a vital role in the U.S. banking system, ensuring accurate and efficient routing of funds between financial institutions. By understanding how ABA numbers work and following best practices for their use, you can streamline your banking processes and protect your financial information.

We encourage you to share this article with others who may benefit from understanding Federal Reserve ABA numbers. If you have any questions or comments, please feel free to leave them below. For more information on banking and finance, explore our other articles on the site.