How to Chase Apply for Mortgage: A Comprehensive Guide

Applying for a mortgage can be a daunting process, but with the right guidance, it can become a manageable and rewarding endeavor. If you're considering applying for a mortgage, understanding the steps involved and the factors that influence your application is crucial. In this article, we will explore how to effectively chase apply for mortgage, ensuring you're well-prepared for the journey ahead.

Whether you're a first-time homebuyer or looking to refinance your current property, the mortgage process involves several key stages. From gathering the necessary documents to understanding interest rates, each step plays a significant role in securing the best mortgage deal for your needs.

This guide will provide you with actionable insights, tips, and expert advice to help you navigate the mortgage application process successfully. Let's dive in and explore everything you need to know about chasing and applying for a mortgage.

Understanding the Mortgage Process

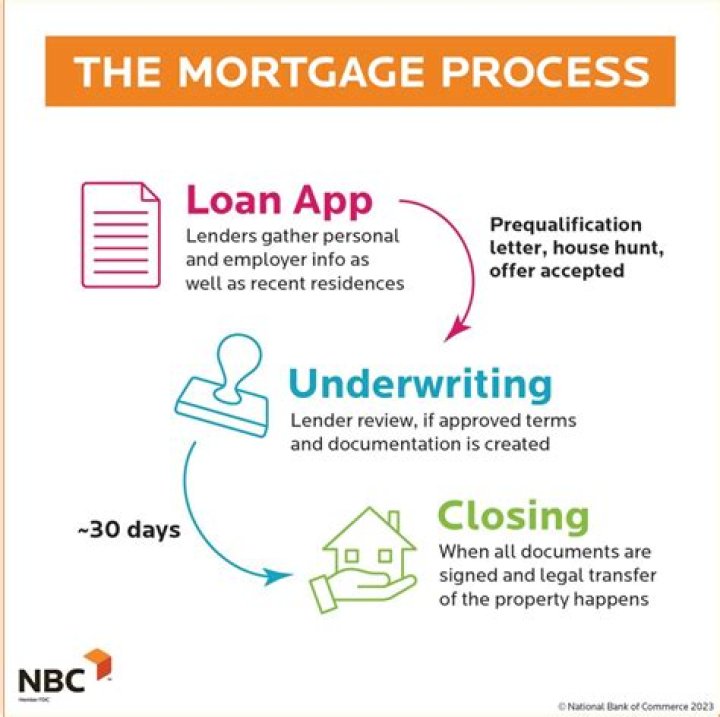

Mortgage applications are a critical step in purchasing a home or refinancing an existing property. To effectively chase apply for mortgage, it's essential to understand the process thoroughly. The mortgage process typically involves several stages, including pre-approval, document submission, underwriting, and closing.

Each stage requires specific actions and documentation to ensure a smooth and successful application. For instance, during the pre-approval stage, lenders evaluate your financial standing to determine how much you can borrow. This step is crucial as it gives you a clear idea of your budget and helps you find homes within your price range.

Understanding the mortgage process empowers you to make informed decisions and prepare adequately for each step. Let's delve deeper into the eligibility requirements for mortgage applications.

Eligibility Requirements for Mortgage

Income Stability

To qualify for a mortgage, you must demonstrate stable income over a period of time. Lenders typically require proof of consistent employment or other reliable sources of income, such as investments or rental income. This ensures that you can meet your monthly mortgage payments without difficulty.

Credit History

Your credit history plays a significant role in determining your eligibility for a mortgage. Lenders review your credit report to assess your financial behavior and reliability in repaying debts. A good credit score increases your chances of securing a favorable mortgage rate.

Debt-to-Income Ratio

Another critical factor in mortgage eligibility is your debt-to-income ratio (DTI). Lenders calculate your DTI by dividing your monthly debt payments by your gross monthly income. A lower DTI indicates better financial health and improves your chances of mortgage approval.

Documents Needed for Mortgage Application

When you decide to chase apply for mortgage, gathering the necessary documents is one of the first steps. Below is a list of essential documents you'll need to prepare:

- Proof of income (pay stubs, W-2 forms, or tax returns)

- Bank statements for the past two months

- Documentation of assets, such as savings accounts or investment portfolios

- Credit report and credit score

- Identification documents (driver's license, passport, or Social Security card)

Having these documents ready will expedite the application process and help you avoid delays.

The Importance of Credit Score

Your credit score is one of the most important factors in the mortgage application process. It influences the interest rates you're offered and the overall terms of your mortgage. A higher credit score indicates lower risk to lenders, resulting in better mortgage terms.

According to the Federal Reserve, maintaining a credit score above 700 can significantly improve your mortgage prospects. However, it's possible to secure a mortgage with a lower score, albeit with less favorable terms. Regularly monitoring your credit report and addressing any discrepancies can help you improve your score over time.

Getting Pre-Approval for Mortgage

Pre-approval is a vital step in the mortgage process. It involves submitting your financial information to a lender for evaluation. Based on this information, the lender provides an estimate of how much you can borrow. Pre-approval offers several benefits:

- It gives you a clearer picture of your budget.

- Sellers are more likely to consider your offer seriously.

- It demonstrates your financial readiness to potential lenders.

While pre-qualification is a preliminary step, pre-approval is a more formal process that involves a thorough review of your financial standing.

Types of Mortgages

Fixed-Rate Mortgage

A fixed-rate mortgage offers a consistent interest rate throughout the loan term, typically 15 or 30 years. This type of mortgage is ideal for borrowers who prefer predictable monthly payments.

Adjustable-Rate Mortgage (ARM)

An adjustable-rate mortgage features an interest rate that changes periodically based on market conditions. While ARMs may start with lower rates, they can increase over time, making them suitable for short-term homeowners.

FHA Mortgage

FHA mortgages are insured by the Federal Housing Administration and are designed for borrowers with lower credit scores or smaller down payments. These mortgages often require a minimum down payment of 3.5%.

Understanding Mortgage Interest Rates

Mortgage interest rates vary based on several factors, including economic conditions, inflation, and the borrower's financial profile. Securing a competitive interest rate can save you thousands of dollars over the life of your loan. Factors influencing interest rates include:

- Your credit score

- The type of mortgage you choose

- Current market conditions

- The loan term

Researching and comparing rates from multiple lenders can help you find the best deal for your mortgage application.

Common Challenges in Mortgage Application

While the mortgage application process is straightforward for many, some borrowers face challenges along the way. Common issues include:

- Poor credit history

- Insufficient down payment

- High debt-to-income ratio

Addressing these challenges early in the process can improve your chances of mortgage approval. For example, improving your credit score or reducing your debt load can significantly enhance your application's strength.

Tips for a Successful Mortgage Application

Here are some practical tips to help you successfully chase apply for mortgage:

- Start building your credit early by paying bills on time and reducing debt.

- Save for a substantial down payment to reduce the loan amount and improve your terms.

- Shop around for lenders and compare their offers to find the best mortgage deal.

- Work with a reputable mortgage broker to guide you through the process.

- Stay organized and keep all necessary documents readily available.

By following these tips, you can streamline the mortgage application process and increase your chances of approval.

Conclusion

Chasing and applying for a mortgage is a significant financial decision that requires careful planning and preparation. By understanding the mortgage process, meeting eligibility requirements, and gathering necessary documents, you can navigate the application process with confidence.

Remember, securing a mortgage is not just about finding the right lender but also about choosing the best terms and rates. Take the time to research, compare options, and consult with financial experts to ensure you make an informed decision.

We invite you to share your thoughts and experiences in the comments below. If you found this guide helpful, consider sharing it with others who may benefit from it. For more insights on mortgage and personal finance, explore our other articles on the site.