What's a Bank ABA Number? A Comprehensive Guide to Understanding and Using It

A bank ABA number, also known as the American Bankers Association routing number, plays a crucial role in facilitating seamless financial transactions across the United States. Whether you're setting up direct deposits, paying bills online, or transferring funds between accounts, understanding what an ABA number is and how it works can save you time and frustration. In this article, we'll explore everything you need to know about bank ABA numbers, from their purpose to their importance in modern banking.

For individuals and businesses alike, navigating the financial system can be overwhelming, especially when dealing with unfamiliar terms. The bank ABA number is one such term that often arises during banking activities. Despite its importance, many people remain unclear about what it is and how it impacts their financial transactions. By the end of this guide, you'll have a thorough understanding of bank ABA numbers and how they streamline banking processes.

In today's digital age, where financial transactions occur at lightning speed, having accurate information about your bank's routing details is essential. This article will walk you through the history, structure, and practical applications of bank ABA numbers, ensuring you're well-prepared for any banking-related task. Let's dive in and uncover the secrets behind this vital banking tool.

What is a Bank ABA Number?

A bank ABA number, or routing transit number (RTN), is a nine-digit code assigned to financial institutions in the United States. This number identifies the specific bank or credit union involved in a transaction. It acts as a digital address, ensuring that funds are routed to the correct institution during transfers. Whether you're setting up direct deposits, paying bills, or initiating wire transfers, the ABA number ensures accuracy and efficiency in financial processes.

ABA numbers are not random; each digit in the sequence serves a specific purpose. These numbers are crucial for domestic transactions within the U.S., distinguishing them from international transaction codes like SWIFT codes. Understanding the structure and function of an ABA number can help you avoid common errors and ensure smooth financial operations.

The History of ABA Numbers

The concept of ABA numbers dates back to 1910 when the American Bankers Association introduced them to standardize check processing. Before this system, checks often faced delays and errors due to inconsistent identification methods. The introduction of ABA numbers revolutionized the banking industry by providing a uniform system for routing financial transactions.

Why Was the ABA Number Created?

- To streamline check processing and reduce errors

- To establish a standardized system for identifying financial institutions

- To improve the efficiency of domestic transactions

Today, ABA numbers remain an integral part of the U.S. financial system, serving as the backbone for various banking activities. Their evolution over the years has kept pace with technological advancements, ensuring their continued relevance in modern banking.

Understanding the Structure of an ABA Number

An ABA number consists of nine digits, each with a specific role in identifying the bank and validating the number. Here's a breakdown of the structure:

- First four digits: Represent the Federal Reserve routing symbol

- Next four digits: Identify the bank or financial institution

- Last digit: Acts as a checksum to validate the number's accuracy

This systematic approach ensures that ABA numbers are both unique and reliable. For example, the ABA number for Bank of America might look like this: 026009593. Each segment of the number provides critical information necessary for successful transactions.

How to Find Your Bank's ABA Number

Locating your bank's ABA number is straightforward and can be done in several ways:

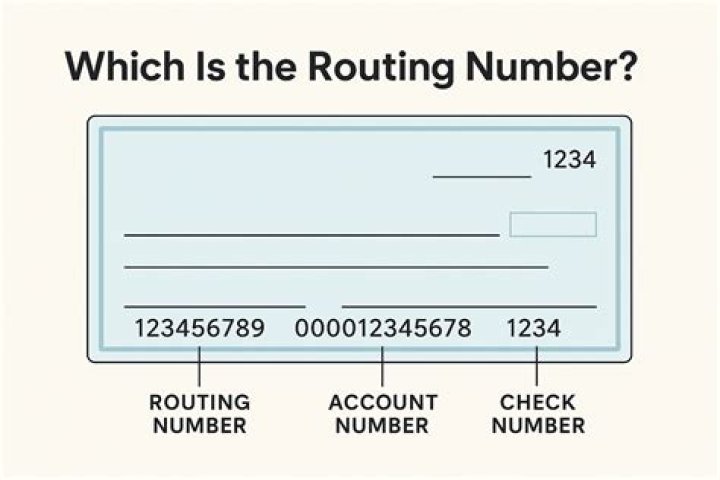

1. Check Your Paper Checks

At the bottom of your personal checks, you'll find a series of numbers. The first set of nine digits on the left is your bank's ABA number. This is the most common and reliable method for identifying your routing number.

2. Visit Your Bank's Website

Most banks provide ABA numbers on their official websites. Simply navigate to the customer support or account information section to find the routing details for your specific account type.

3. Contact Customer Service

If you're unable to locate your ABA number through other means, reach out to your bank's customer service team. They can provide the correct number based on your account details.

Regardless of the method you choose, ensure that the ABA number matches the one associated with your specific account to avoid transaction errors.

Common Uses of ABA Numbers

ABA numbers serve multiple purposes in the banking world. Here are some of the most common applications:

- Direct Deposits: Used to route salary payments or government benefits directly into your account

- Bill Payments: Facilitates automatic payments for utilities, loans, and other recurring expenses

- Funds Transfers: Enables seamless transfers between accounts at the same or different banks

- Tax Payments: Helps you submit federal or state tax payments electronically

Each of these applications relies on accurate ABA numbers to ensure that funds are directed to the correct destination without delays or errors.

ABA Numbers vs. SWIFT Codes: Key Differences

While ABA numbers and SWIFT codes both serve to route financial transactions, they differ significantly in scope and application:

ABA Numbers

- Used exclusively for domestic transactions within the U.S.

- Consist of nine digits

- Identify specific banks or credit unions

SWIFT Codes

- Used for international transactions

- Consist of 8-11 alphanumeric characters

- Identify global financial institutions

Understanding the distinction between these two systems is essential for ensuring that you use the correct code for your transaction type.

Security Measures for ABA Numbers

While ABA numbers are essential for financial transactions, they also pose potential security risks if misused. Here are some best practices to protect your ABA number:

- Keep it Private: Share your ABA number only with trusted entities

- Verify Recipients: Double-check the recipient's details before initiating a transfer

- Monitor Accounts: Regularly review your bank statements for unauthorized transactions

By following these security measures, you can minimize the risk of fraud and protect your financial information.

Common Errors and How to Avoid Them

Mistakes involving ABA numbers can lead to significant delays or even lost funds. Here are some common errors and tips to avoid them:

- Transposing Digits: Double-check the sequence of numbers to ensure accuracy

- Using the Wrong Number: Confirm that the ABA number matches your specific account type

- Ignoring Confirmation Emails: Always review transaction confirmations to verify details

Attention to detail can save you from costly mistakes and ensure smooth financial operations.

ABA Numbers for Major Banks in the U.S.

Here's a list of ABA numbers for some of the largest banks in the United States:

- Bank of America: 026009593

- Chase Bank: 021000021

- Wells Fargo: 121000248

- Citibank: 021000089

Remember that ABA numbers may vary depending on the account type and location, so always confirm the correct number with your bank.

Conclusion: Why Knowing Your ABA Number Matters

In conclusion, understanding what a bank ABA number is and how it functions is essential for anyone involved in U.S. banking. From facilitating direct deposits to ensuring secure fund transfers, ABA numbers play a critical role in modern financial transactions. By following the tips and best practices outlined in this guide, you can ensure accurate and efficient banking experiences.

We encourage you to share this article with friends and family to help them navigate the world of banking with confidence. If you have any questions or feedback, please leave a comment below. And don't forget to explore our other articles for more valuable insights into personal finance and banking!