What Does ABA in Banking Stand For? A Comprehensive Guide

When it comes to banking terminology, one term that often arises is ABA. The term ABA plays a crucial role in banking operations and financial transactions. Understanding what ABA stands for in banking and its significance can help individuals manage their finances more effectively. In this article, we will explore the meaning of ABA in banking, its functions, and why it is important in the financial world.

Banking has evolved significantly over the years, and with the rise of digital transactions, understanding key terms like ABA is more important than ever. Whether you're managing your personal finances or working in the financial industry, knowing what ABA represents is essential for smooth transactions.

Throughout this article, we will delve into the history of ABA, its applications in banking, and how it affects everyday banking activities. By the end of this guide, you will have a clear understanding of the importance of ABA in banking and how it contributes to the efficiency of financial systems.

What Does ABA Stand For in Banking?

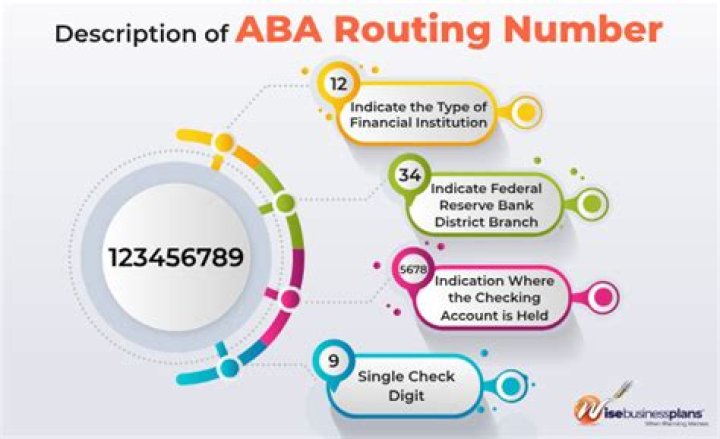

ABA stands for American Bankers Association. It is a unique identification number assigned to financial institutions in the United States. This number plays a critical role in facilitating electronic transactions, such as direct deposits, wire transfers, and automated clearing house (ACH) transactions. The ABA number ensures that funds are routed to the correct bank or financial institution.

Importance of ABA Numbers in Transactions

ABA numbers are crucial for ensuring the accuracy and security of financial transactions. Without an ABA number, banks would face difficulties in processing payments and transfers efficiently. These numbers serve as a digital address for banks, allowing them to communicate with one another seamlessly.

History of ABA in Banking

The concept of ABA numbers originated in 1910 when the American Bankers Association introduced them to standardize the routing of checks and financial transactions. Over the years, the use of ABA numbers has expanded to include electronic transactions, making them an indispensable part of modern banking.

Evolution of ABA in the Digital Age

With the advent of digital banking, the role of ABA numbers has become even more significant. They are now used in various electronic payment systems, ensuring that transactions are processed quickly and securely. The evolution of ABA numbers reflects the broader transformation of the banking industry.

Key Functions of ABA in Banking

The primary function of an ABA number is to identify financial institutions and facilitate transactions. Below are some of the key functions of ABA numbers in banking:

- Routing Payments: ABA numbers ensure that payments are directed to the correct bank or financial institution.

- Direct Deposits: Employers use ABA numbers to deposit salaries directly into employees' bank accounts.

- Wire Transfers: ABA numbers are essential for executing domestic wire transfers.

- ACH Transactions: ABA numbers are used in automated clearing house transactions, such as bill payments and tax refunds.

Types of ABA Numbers

There are two main types of ABA numbers used in banking:

1. Paper-Based ABA Numbers

These numbers are used for processing paper checks and other physical transactions. They are typically found at the bottom of checks and are essential for check clearing processes.

2. Electronic ABA Numbers

Electronic ABA numbers are used for digital transactions, including wire transfers and ACH payments. These numbers are often different from paper-based ABA numbers and are used exclusively for electronic transactions.

Why Is ABA Important in Banking?

ABA numbers are vital for maintaining the integrity and efficiency of the banking system. They provide a standardized method for identifying financial institutions and ensuring that transactions are processed accurately. Without ABA numbers, the banking system would face significant challenges in routing payments and executing transactions.

Impact on Financial Stability

The use of ABA numbers contributes to the stability of the financial system by reducing errors and fraud in transactions. By providing a unique identifier for each bank, ABA numbers help prevent unauthorized access and ensure that funds are transferred securely.

How ABA Numbers Are Used

ABA numbers are used in various banking activities, including:

- Check Processing: ABA numbers are printed on checks to identify the bank and account associated with the transaction.

- Wire Transfers: Individuals and businesses use ABA numbers to send and receive funds electronically.

- Direct Deposits: Employers use ABA numbers to deposit salaries directly into employees' accounts.

- Bill Payments: Consumers use ABA numbers to set up automatic bill payments through ACH transactions.

ABA and Security in Banking

Security is a top priority in banking, and ABA numbers play a crucial role in ensuring the safety of financial transactions. Banks use advanced encryption and authentication methods to protect ABA numbers and prevent unauthorized access.

Best Practices for Protecting ABA Numbers

To safeguard your ABA number and prevent fraud, consider the following best practices:

- Keep your ABA number confidential and avoid sharing it unnecessarily.

- Use secure methods for transmitting ABA numbers, such as encrypted email or secure online portals.

- Monitor your bank account regularly for suspicious activity and report any discrepancies immediately.

Challenges Related to ABA in Banking

Despite their importance, ABA numbers are not without challenges. Some of the common issues associated with ABA numbers include:

- Human Error: Mistakes in entering ABA numbers can lead to failed transactions or delays in processing.

- Fraud: Criminals may attempt to use stolen ABA numbers to commit financial fraud.

- System Compatibility: Differences in ABA number formats between paper-based and electronic systems can cause complications.

Addressing These Challenges

Banks and financial institutions are continually working to address these challenges by implementing advanced technologies and security measures. Educating customers about the proper use and protection of ABA numbers is also essential for minimizing risks.

The Future of ABA in Banking

As technology continues to evolve, the role of ABA numbers in banking is likely to expand. Innovations such as blockchain and artificial intelligence may transform the way ABA numbers are used in financial transactions. Despite these changes, ABA numbers will remain a fundamental component of the banking system for the foreseeable future.

Emerging Technologies and ABA Numbers

Emerging technologies like real-time payment systems and digital currencies may require new approaches to ABA numbers. However, their core function of identifying financial institutions and facilitating transactions will remain unchanged.

Conclusion and Call to Action

In conclusion, ABA numbers are an integral part of the banking system, ensuring the accuracy and security of financial transactions. Understanding what ABA stands for in banking and its significance can help individuals and businesses manage their finances more effectively.

We encourage you to share this article with others who may benefit from learning about ABA numbers in banking. For more information on financial topics, explore our other articles and resources. If you have any questions or comments, feel free to leave them below. Together, let's build a more informed and secure financial future!

Data Sources: FDIC, Federal Reserve, American Bankers Association