What is ABA Number Bank: A Comprehensive Guide

Understanding the ABA number bank is essential for anyone who frequently engages in banking transactions, especially those involving direct deposits, wire transfers, or check processing. The ABA number, also known as the American Bankers Association routing number, serves as a unique identifier for banks and financial institutions within the United States. This number ensures that funds are routed to the correct institution, preventing errors in transactions.

As technology continues to evolve, the importance of understanding ABA numbers has grown significantly. Whether you're setting up automatic bill payments, transferring money between accounts, or receiving your salary through direct deposit, knowing how ABA numbers work can save you from potential financial mishaps.

This article aims to provide a detailed explanation of what an ABA number is, its purpose, and how it functions in the banking system. By the end of this guide, you'll have a thorough understanding of ABA numbers and their significance in modern banking.

What is an ABA Number?

An ABA number, or American Bankers Association routing number, is a nine-digit code used to identify financial institutions in the United States. It was originally developed in 1910 by the American Bankers Association to facilitate the accurate processing of paper checks. Over time, its use has expanded to include electronic funds transfers, direct deposits, and other financial transactions.

This number acts as a digital address for banks, ensuring that money is directed to the correct institution during transactions. Without an ABA number, the banking system would face significant challenges in processing payments efficiently and securely.

How ABA Numbers Work

When you initiate a transaction, such as setting up direct deposit or sending money to another account, the ABA number is used to verify the identity of the bank involved. This ensures that the funds are sent to the correct institution and account holder.

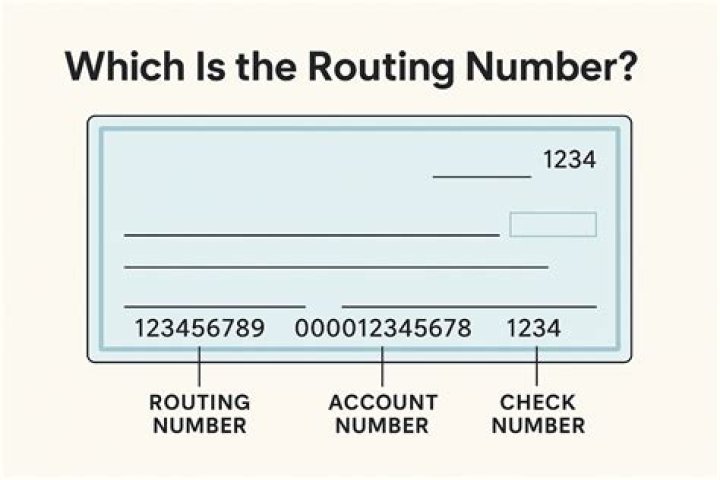

Structure of an ABA Number

An ABA number consists of nine digits, each serving a specific purpose. Understanding the structure of an ABA number can help you verify its authenticity and avoid errors in transactions.

Breaking Down the Nine Digits

- First four digits: Represent the Federal Reserve Routing Symbol, which indicates the Federal Reserve Bank where the institution holds an account.

- Next four digits: Identify the specific financial institution.

- Ninth digit: Acts as a checksum digit, calculated using a specific formula to ensure the number's validity.

This structure ensures that every ABA number is unique and verifiable, reducing the risk of errors in financial transactions.

Purpose of ABA Numbers

The primary purpose of ABA numbers is to streamline the processing of financial transactions. By providing a standardized system for identifying banks, ABA numbers help ensure that funds are transferred accurately and efficiently.

Key Functions of ABA Numbers

- Facilitating check processing and clearing.

- Enabling direct deposits and automatic bill payments.

- Supporting electronic funds transfers between accounts.

- Verifying the identity of financial institutions during transactions.

Without ABA numbers, the banking system would face significant challenges in processing payments securely and efficiently.

How to Find Your ABA Number

Finding your ABA number is a straightforward process. Depending on your needs, there are several methods you can use to locate this important information.

Methods for Finding Your ABA Number

- Check your checks: The ABA number is printed on the bottom left corner of your checks.

- Online banking: Many banks provide your ABA number in the account details section of their online banking platforms.

- Contact customer service: If you're unable to find your ABA number, you can contact your bank's customer service for assistance.

By using one of these methods, you can easily obtain your ABA number and ensure that your transactions are processed correctly.

Common Uses of ABA Numbers

ABA numbers are used in a variety of financial transactions, making them an essential component of the modern banking system. Below are some of the most common uses of ABA numbers:

Key Applications of ABA Numbers

- Direct deposits: Employers use ABA numbers to deposit salaries directly into employees' bank accounts.

- Electronic funds transfers (EFT): ABA numbers are used to transfer funds between accounts at different banks.

- Bill payments: Many companies use ABA numbers to process automatic bill payments on behalf of their customers.

- Check processing: ABA numbers ensure that checks are cleared and funds are transferred to the correct bank.

These applications demonstrate the versatility and importance of ABA numbers in facilitating financial transactions.

ABA vs. SWIFT Codes

While ABA numbers and SWIFT codes both serve to identify financial institutions, they differ in their scope and application. Understanding these differences can help you choose the right code for your transaction needs.

Key Differences Between ABA Numbers and SWIFT Codes

- Scope: ABA numbers are used exclusively within the United States, while SWIFT codes are used globally.

- Purpose: ABA numbers are primarily used for domestic transactions, whereas SWIFT codes are used for international transfers.

- Structure: ABA numbers consist of nine digits, while SWIFT codes are alphanumeric and can range from 8 to 11 characters.

Choosing the appropriate code depends on the nature of your transaction and the location of the involved financial institutions.

History of ABA Numbers

The history of ABA numbers dates back to 1910, when the American Bankers Association introduced the routing number system to improve the efficiency of check processing. Over the years, the system has evolved to accommodate new technologies and transaction methods, ensuring its continued relevance in the modern banking landscape.

Key Milestones in ABA Number History

- 1910: The ABA routing number system is introduced to streamline check processing.

- 1950s: Magnetic Ink Character Recognition (MICR) technology is developed, allowing for automated check processing using ABA numbers.

- 2000s: The rise of electronic banking expands the use of ABA numbers beyond check processing to include direct deposits and EFTs.

This evolution highlights the adaptability and importance of ABA numbers in the banking industry.

ABA Number Security

While ABA numbers are essential for facilitating financial transactions, they must also be handled securely to prevent fraud and unauthorized access. Implementing best practices for ABA number security can help protect your accounts and personal information.

Tips for Securing Your ABA Number

- Keep it confidential: Avoid sharing your ABA number unnecessarily, especially online or over the phone.

- Monitor transactions: Regularly review your bank statements to detect any suspicious activity.

- Use secure channels: When providing your ABA number for transactions, ensure you're using a secure and reputable platform.

By following these tips, you can help safeguard your ABA number and protect your financial information.

Common Challenges with ABA Numbers

Despite their importance, ABA numbers can present challenges for both consumers and financial institutions. Understanding these challenges can help you navigate potential issues and ensure smooth transactions.

Common Issues with ABA Numbers

- Incorrect entry: Entering the wrong ABA number can result in delayed or failed transactions.

- Security risks: Sharing your ABA number with unauthorized parties can expose you to fraud and identity theft.

- System limitations: Some older systems may not support the full range of ABA number functionalities, leading to processing delays.

Addressing these challenges requires vigilance, secure practices, and collaboration between consumers and financial institutions.

The Future of ABA Numbers

As the banking industry continues to evolve, the role of ABA numbers is likely to expand and adapt to new technologies and transaction methods. Innovations in digital banking, blockchain, and artificial intelligence may further enhance the functionality and security of ABA numbers in the years to come.

By staying informed about these developments, consumers and financial institutions can ensure that ABA numbers continue to play a vital role in facilitating secure and efficient financial transactions.

Conclusion

In conclusion, understanding what an ABA number is and how it functions is crucial for anyone involved in banking transactions. From facilitating direct deposits and electronic transfers to ensuring check processing accuracy, ABA numbers serve as the backbone of the modern banking system.

We encourage you to share your thoughts and experiences with ABA numbers in the comments section below. Additionally, feel free to explore other articles on our site for more insights into banking and finance. Together, let's continue to build a more informed and secure financial future.