What is an ABA Number? A Comprehensive Guide to Understanding ABA Routing Numbers

In today's digital banking era, understanding the intricacies of financial systems is crucial. One essential component of banking transactions is the ABA number. If you're wondering, "What is an ABA number?" you're in the right place. This article will provide an in-depth explanation of ABA numbers, their purpose, and how they function within the banking system.

As financial transactions become increasingly digital, it's vital to comprehend the infrastructure that facilitates these processes. ABA numbers play a pivotal role in ensuring seamless transactions between financial institutions.

This guide will help you understand what an ABA number is, its significance, and how it affects your banking activities. Whether you're a business owner or an individual managing personal finances, this information will empower you to navigate banking systems more effectively.

ABA Number Basics

An ABA number, also known as a routing transit number (RTN), is a nine-digit code used by financial institutions in the United States to identify themselves. This number is essential for processing checks, wire transfers, and other financial transactions. Banks and credit unions use ABA numbers to ensure that funds are routed to the correct institution.

When you're setting up direct deposits, automatic payments, or transferring money between accounts, the ABA number ensures that the transaction is directed to the right bank. Without this number, financial transactions could be delayed or sent to the wrong institution.

How ABA Numbers Work

ABA numbers function as a unique identifier for banks and credit unions. When a transaction is initiated, the ABA number is used to determine the financial institution involved in the transaction. This ensures that funds are transferred accurately and efficiently.

The History of ABA Numbers

The American Bankers Association (ABA) introduced ABA numbers in 1910 to standardize the process of identifying banks and routing transactions. At the time, the banking system was becoming more complex, and a standardized method was needed to streamline operations.

Since its inception, the ABA number has evolved to accommodate advancements in technology and changes in the financial landscape. Today, it remains a critical component of the banking infrastructure in the United States.

Evolution of ABA Numbers

- 1910: ABA numbers were first introduced.

- 1940s: The numbers were adopted for check processing.

- 1970s: The system expanded to include electronic transactions.

- Present day: ABA numbers are used for a wide range of financial transactions.

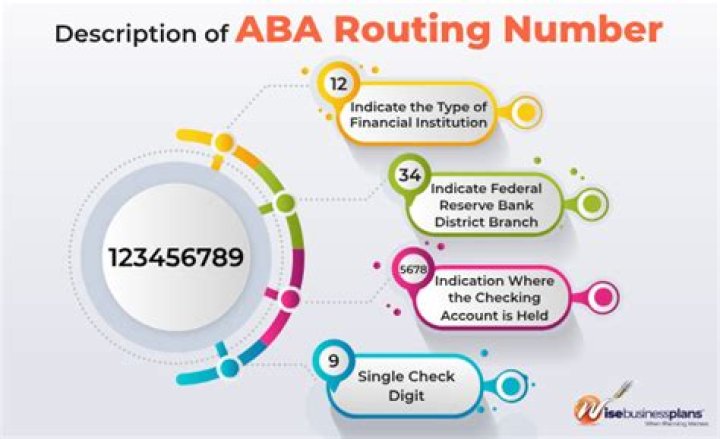

Structure of an ABA Number

An ABA number consists of nine digits, each serving a specific purpose:

- The first four digits identify the Federal Reserve routing symbol.

- The next four digits represent the bank's or credit union's unique identifier.

- The final digit is a check digit used to verify the validity of the ABA number.

For example, an ABA number like 123456789 can be broken down as follows:

- 1234: Federal Reserve routing symbol

- 5678: Bank or credit union identifier

- 9: Check digit

Uses of ABA Numbers

ABA numbers are used in various financial transactions, including:

- Direct deposits

- Wire transfers

- Automatic bill payments

- Check processing

- ACH (Automated Clearing House) transactions

Each of these transactions relies on the ABA number to ensure that funds are routed to the correct institution. Without this number, the financial system would face significant delays and errors.

How to Find Your ABA Number

Locating your ABA number is straightforward. Here are a few methods:

- Check: The ABA number is printed on the bottom left corner of your checks.

- Bank Statement: Your ABA number may be listed on your monthly bank statement.

- Bank Website: Many banks provide ABA numbers on their websites for customer convenience.

- Customer Service: Contact your bank's customer service department for assistance in finding your ABA number.

Tips for Verifying Your ABA Number

When verifying your ABA number, ensure that you're using the correct number for the type of transaction you're conducting. Some banks have different ABA numbers for wire transfers and ACH transactions.

ABA vs. ACH Numbers

While ABA numbers and ACH numbers are often used interchangeably, they serve different purposes:

- ABA Number: A unique identifier for a bank or credit union used in routing transactions.

- ACH Number: A number used specifically for electronic transactions processed through the Automated Clearing House network.

For most transactions, the ABA number and ACH number are the same. However, some banks use different numbers for wire transfers and ACH transactions, so it's important to confirm which number to use based on the transaction type.

Differences Between ABA and ACH Transactions

ABA numbers are used for a broader range of transactions, while ACH numbers are specifically designed for electronic transfers. Understanding the distinction can help you ensure that your transactions are processed correctly.

Why ABA Numbers Are Important

ABA numbers are crucial for maintaining the integrity and efficiency of the financial system. They ensure that funds are routed to the correct institution, reducing the risk of errors and delays. Additionally, ABA numbers help prevent fraud by providing a standardized method for identifying financial institutions.

For businesses and individuals alike, understanding ABA numbers is essential for managing finances effectively. Whether you're setting up direct deposits, paying bills automatically, or transferring money between accounts, the ABA number plays a vital role in ensuring that your transactions are processed accurately.

ABA Number Security

While ABA numbers are essential for financial transactions, they must be handled with care to protect sensitive information. Sharing your ABA number with unauthorized parties can lead to fraud or unauthorized access to your accounts.

To safeguard your ABA number:

- Only share it with trusted institutions or individuals.

- Be cautious when providing your ABA number online or over the phone.

- Monitor your accounts regularly for suspicious activity.

Common Questions About ABA Numbers

Q1: Can I use the same ABA number for all transactions?

Not necessarily. Some banks have different ABA numbers for wire transfers and ACH transactions. Always confirm which number to use based on the transaction type.

Q2: What happens if I use the wrong ABA number?

Using the wrong ABA number can result in delayed or failed transactions. It's crucial to verify the correct number before initiating any financial transaction.

Q3: Are ABA numbers unique to each bank?

Yes, ABA numbers are unique identifiers assigned to each financial institution. This ensures that transactions are routed to the correct bank or credit union.

Conclusion

Understanding what an ABA number is and its role in the financial system is essential for managing your finances effectively. From facilitating seamless transactions to ensuring the security of your accounts, ABA numbers play a critical role in modern banking.

We encourage you to take action by reviewing your ABA number and ensuring that it's accurate for all your financial transactions. If you have further questions or need clarification, feel free to leave a comment below. Additionally, explore our other articles for more insights into financial management and banking systems.

Remember, staying informed about financial tools like ABA numbers empowers you to make better financial decisions. Share this article with others who may benefit from understanding the importance of ABA numbers in banking transactions.