What is Routing ABA Number: A Comprehensive Guide

Routing ABA numbers play a crucial role in the banking industry, serving as a unique identifier for financial institutions in the United States. These numbers ensure that transactions are processed accurately and efficiently. Understanding what a routing ABA number is can help individuals and businesses navigate their financial operations with ease.

For anyone who has ever processed a check, transferred funds, or set up direct deposits, you've likely encountered routing ABA numbers. These codes, while small in appearance, carry significant importance in facilitating seamless financial transactions. This article dives deep into the world of routing ABA numbers, uncovering their purpose, structure, and applications.

Whether you're a business owner, an individual managing personal finances, or simply curious about the inner workings of banking systems, this guide will provide valuable insights. We'll explore everything from the history of routing ABA numbers to their practical uses today, ensuring you leave with a thorough understanding of this essential banking tool.

History of Routing ABA Numbers

The American Bankers Association (ABA) introduced routing numbers in 1910 to streamline the processing of checks. Before this, checks were manually sorted, which was time-consuming and prone to errors. The introduction of routing ABA numbers revolutionized the banking system, allowing for faster and more accurate processing of financial transactions.

This innovation laid the foundation for modern banking practices. Over the years, the use of routing ABA numbers has expanded beyond check processing to include electronic funds transfers, direct deposits, and other financial operations. The evolution of these numbers reflects the growing complexity and sophistication of the financial industry.

Today, routing ABA numbers remain a vital component of the U.S. banking system, ensuring that transactions are routed to the correct financial institution. Understanding their historical context provides valuable insight into their continued relevance and importance.

Structure of an ABA Routing Number

Components of an ABA Routing Number

An ABA routing number consists of nine digits, each with a specific purpose. The first four digits represent the Federal Reserve Routing Symbol, indicating the Federal Reserve Bank responsible for processing the transaction. The next four digits identify the specific financial institution, while the final digit serves as a checksum to ensure the number's validity.

- Federal Reserve Routing Symbol: Identifies the Federal Reserve Bank.

- Financial Institution Identifier: Specifies the bank or credit union.

- Checksum Digit: Validates the routing number's accuracy.

This structure ensures that each routing ABA number is unique and can be accurately verified. Understanding the components of a routing ABA number is essential for anyone involved in financial transactions.

Purposes and Uses of Routing ABA Numbers

Routing ABA numbers serve a variety of purposes in the financial industry. They are primarily used for processing checks, but their applications extend to electronic funds transfers, direct deposits, and automated clearing house (ACH) transactions. These numbers ensure that funds are directed to the correct account and financial institution.

For businesses, routing ABA numbers facilitate payroll processing and vendor payments. Individuals use them to set up direct deposits for salaries, pensions, and government benefits. The versatility of routing ABA numbers makes them an indispensable tool in modern finance.

As financial technology continues to evolve, the importance of routing ABA numbers remains unchanged. They provide the foundation for secure and efficient financial transactions, ensuring that money moves where it needs to go.

How to Verify an ABA Routing Number

Steps to Verify a Routing ABA Number

Verifying an ABA routing number is crucial to prevent errors and fraud in financial transactions. The process involves checking the checksum digit to ensure the number's validity. Financial institutions often provide tools or resources to assist with this verification.

- Check the checksum digit using a verification formula.

- Contact your bank or credit union for confirmation.

- Use online resources or databases designed for routing number verification.

By following these steps, individuals and businesses can ensure the accuracy of routing ABA numbers, reducing the risk of transaction errors and enhancing financial security.

Differences Between ABA and ACH Routing Numbers

While ABA and ACH routing numbers may seem similar, they serve distinct purposes in the financial system. ABA routing numbers are primarily used for check processing, while ACH routing numbers are designed for electronic funds transfers. Understanding the differences between these numbers is essential for managing various types of transactions.

ABA routing numbers are typically printed on checks, while ACH routing numbers may differ for electronic transactions. Some financial institutions use the same number for both purposes, while others provide separate numbers for ABA and ACH transactions. It's important to confirm which number to use based on the transaction type.

By recognizing the distinctions between ABA and ACH routing numbers, individuals and businesses can ensure that their transactions are processed correctly and efficiently.

Security Concerns and Safeguards

Protecting Routing ABA Numbers from Fraud

Routing ABA numbers are sensitive information that, if misused, can lead to financial fraud. It's crucial to safeguard these numbers to protect against unauthorized transactions and identity theft. Financial institutions employ various measures to ensure the security of routing ABA numbers.

- Use secure connections when sharing routing numbers online.

- Limit access to routing numbers to trusted individuals or entities.

- Regularly monitor accounts for suspicious activity.

By implementing these safeguards, individuals and businesses can minimize the risk of fraud and maintain the integrity of their financial transactions.

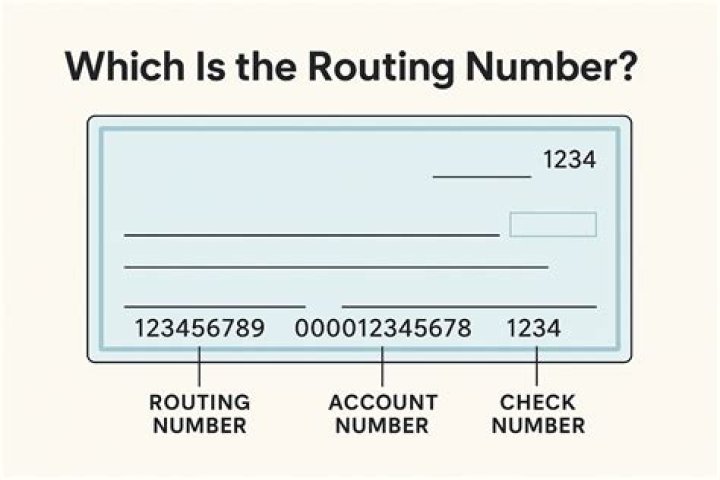

How to Find Your ABA Routing Number

Finding your ABA routing number is a straightforward process. For check transactions, the number is printed at the bottom of your checks, typically the first set of numbers on the left. Alternatively, you can obtain your routing ABA number by contacting your bank or credit union directly.

Many financial institutions also provide online access to routing numbers through their websites or mobile apps. This convenience allows users to retrieve their numbers quickly and securely. Whether you're processing checks or setting up electronic transfers, knowing how to find your routing ABA number is essential for managing your finances effectively.

International Transactions and ABA Routing Numbers

While routing ABA numbers are primarily used within the United States, they can play a role in international transactions. For example, foreign banks may require a routing ABA number when sending funds to a U.S.-based account. However, it's important to note that routing numbers alone may not suffice for cross-border transactions.

International transactions often involve additional identifiers, such as SWIFT codes, to ensure accurate processing. Understanding the role of routing ABA numbers in global finance is crucial for anyone involved in international banking operations.

By recognizing the limitations and applications of routing ABA numbers in international contexts, individuals and businesses can navigate global transactions with confidence.

Regulations Surrounding ABA Routing Numbers

Compliance and Oversight of Routing ABA Numbers

Routing ABA numbers are subject to strict regulations to ensure their proper use and security. The American Bankers Association and the Federal Reserve oversee the assignment and management of these numbers, enforcing compliance with industry standards.

Financial institutions must adhere to these regulations to maintain the integrity of the routing ABA system. Regular audits and updates ensure that routing numbers remain accurate and secure. Understanding the regulatory framework surrounding routing ABA numbers is essential for anyone involved in financial transactions.

By following these regulations, financial institutions can provide a secure and reliable environment for processing transactions.

The Future of Routing ABA Numbers

As technology continues to advance, the role of routing ABA numbers in the financial industry is likely to evolve. Innovations in digital banking and payment systems may introduce new methods for processing transactions, potentially altering the traditional use of routing numbers.

Despite these changes, routing ABA numbers will likely remain a fundamental component of the U.S. banking system. Their adaptability and reliability ensure their continued relevance in facilitating secure and efficient financial transactions.

By staying informed about developments in the financial industry, individuals and businesses can prepare for the future of routing ABA numbers and their impact on modern banking practices.

Conclusion

In conclusion, routing ABA numbers are a critical component of the U.S. banking system, ensuring the accuracy and security of financial transactions. From their historical origins to their modern applications, these numbers have played a vital role in shaping the financial industry.

Understanding the structure, purposes, and security measures associated with routing ABA numbers is essential for anyone involved in financial operations. By following the guidelines and best practices outlined in this article, individuals and businesses can manage their finances with confidence and efficiency.

We invite you to share your thoughts and experiences with routing ABA numbers in the comments section below. Additionally, feel free to explore other articles on our site for more insights into the world of finance and banking. Together, let's navigate the complexities of modern banking with knowledge and expertise.