What is the ABA Number for a Bank: A Comprehensive Guide

Understanding the ABA number for a bank is crucial for anyone who engages in financial transactions, especially when it comes to direct deposits, wire transfers, or check processing. This unique routing code ensures that your money reaches the right destination safely and efficiently. In this article, we will delve into the intricacies of ABA numbers, their importance, and how they function within the banking system.

Whether you're setting up a direct deposit for your paycheck or initiating an electronic funds transfer, knowing your bank's ABA number is essential. It acts as a digital address for banks, ensuring seamless communication and accurate fund transfers between financial institutions.

This article is designed to provide a detailed and comprehensive overview of ABA numbers, including their history, structure, and applications. We'll also explore how to locate your bank's ABA number and address common questions that arise when dealing with this critical banking component.

Introduction to ABA Numbers

The American Bankers Association (ABA) routing number, commonly referred to as the ABA number, is a nine-digit code assigned to financial institutions in the United States. It serves as a unique identifier for banks and helps streamline the processing of financial transactions.

Why ABA Numbers Are Important

ABA numbers are indispensable for various banking activities, including:

- Direct deposits

- Automated Clearing House (ACH) transactions

- Wire transfers

- Check processing

Without an ABA number, banks would face significant challenges in ensuring that funds are transferred accurately and securely.

History and Evolution of ABA Numbers

The concept of ABA numbers dates back to 1910 when the American Bankers Association introduced the routing transit number system to simplify check processing. Over the years, the system has evolved to accommodate the growing complexity of modern banking operations.

Key Milestones in ABA Number Development

Here are some significant milestones in the evolution of ABA numbers:

- 1910: The first ABA numbers were introduced to facilitate check processing.

- 1950s: Magnetic Ink Character Recognition (MICR) technology was developed, allowing for faster processing of checks.

- 1970s: The rise of electronic banking led to the adoption of ABA numbers for electronic funds transfers.

Structure of an ABA Number

An ABA number consists of nine digits, each serving a specific purpose:

- First four digits: Represent the Federal Reserve routing symbol.

- Fifth and sixth digits: Indicate the American Bankers Association institution identifier.

- Seventh digit: Identifies the check-digit, which is used to verify the accuracy of the ABA number.

- Last two digits: Represent the bank's unique identifier.

This structure ensures that ABA numbers are both unique and verifiable.

How to Validate an ABA Number

Validating an ABA number involves using a check-digit algorithm to confirm its accuracy. This process helps prevent errors and fraudulent activity in financial transactions.

Functions of ABA Numbers

ABA numbers play a critical role in various banking functions:

- Facilitating direct deposits for paychecks and government benefits.

- Enabling electronic funds transfers through the Automated Clearing House (ACH) network.

- Processing checks by identifying the bank responsible for honoring the payment.

These functions highlight the importance of ABA numbers in maintaining the efficiency and security of the banking system.

Role in Modern Banking

With the increasing reliance on digital banking services, ABA numbers have become even more essential. They ensure that transactions are processed accurately and securely, regardless of the method used.

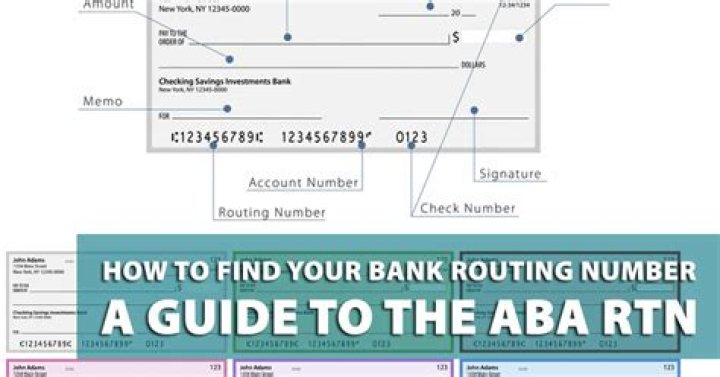

How to Locate Your Bank's ABA Number

Locating your bank's ABA number is straightforward and can be done in several ways:

- Bank statement: Your bank's ABA number is typically listed on your monthly statement.

- Online banking: Most banks provide access to ABA numbers through their online banking platforms.

- Checkbook: The ABA number is printed on the bottom left corner of your checks.

- Customer service: Contact your bank's customer service department for assistance in locating your ABA number.

By using these methods, you can easily obtain your bank's ABA number for your financial transactions.

Tips for Verifying Your ABA Number

When verifying your ABA number, ensure that it matches the one listed on your bank's official website or statement. This step helps prevent errors and ensures the accuracy of your transactions.

ABA vs. SWIFT Codes

While ABA numbers and SWIFT codes both serve to facilitate financial transactions, they differ in several key aspects:

- Purpose: ABA numbers are primarily used for domestic transactions, while SWIFT codes are used for international transfers.

- Structure: ABA numbers consist of nine digits, whereas SWIFT codes are alphanumeric and vary in length.

- Scope: ABA numbers are specific to the United States, while SWIFT codes are used globally.

Understanding these differences is crucial for selecting the appropriate code for your banking needs.

Choosing the Right Code for Your Transactions

When initiating a financial transaction, consider the nature of the transfer and the location of the involved parties. For domestic transfers within the U.S., an ABA number is sufficient. For international transfers, a SWIFT code is required.

Security Concerns with ABA Numbers

While ABA numbers are generally secure, there are potential risks associated with their misuse:

- Fraud: Unauthorized use of ABA numbers can lead to fraudulent transactions.

- Identity theft: Sharing ABA numbers carelessly may expose sensitive financial information.

To mitigate these risks, always verify the authenticity of the ABA number and avoid sharing it unnecessarily.

Best Practices for Protecting Your ABA Number

Implementing the following best practices can help safeguard your ABA number:

- Store your ABA number in a secure location.

- Limit sharing to trusted parties involved in legitimate transactions.

- Monitor your bank account regularly for any suspicious activity.

Common Uses of ABA Numbers

ABA numbers are widely used in various banking scenarios:

- Direct deposits: Employers use ABA numbers to deposit employee paychecks directly into their bank accounts.

- Bill payments: Consumers can use ABA numbers to set up automatic bill payments for utilities, loans, and other recurring expenses.

- Peer-to-peer transfers: ABA numbers enable secure transfers between individuals through platforms like Zelle or Venmo.

These applications demonstrate the versatility and importance of ABA numbers in everyday banking activities.

Emerging Technologies and ABA Numbers

As technology continues to evolve, ABA numbers are adapting to new platforms and systems. For instance, mobile banking apps now allow users to initiate transactions using ABA numbers with just a few taps on their smartphones.

Frequently Asked Questions About ABA Numbers

What happens if I provide the wrong ABA number?

Providing an incorrect ABA number can result in failed or delayed transactions. It is crucial to double-check the ABA number before initiating any financial transfer.

Can I use the same ABA number for multiple transactions?

Yes, ABA numbers are reusable and can be used for multiple transactions involving the same bank account.

Are ABA numbers the same as routing numbers?

Yes, ABA numbers and routing numbers are interchangeable terms used to describe the nine-digit code assigned to financial institutions.

Conclusion

In conclusion, understanding the ABA number for a bank is essential for anyone engaging in financial transactions within the United States. From facilitating direct deposits to enabling electronic funds transfers, ABA numbers play a vital role in ensuring the accuracy and security of banking operations.

We encourage you to share this article with others who may benefit from learning about ABA numbers. If you have any questions or comments, feel free to leave them below. Additionally, explore our other articles for more insights into the world of finance and banking.

Data Source: Federal Reserve | American Bankers Association