Understanding Chase FHA Loan Credit Score Requirements: A Comprehensive Guide

Chase FHA loan credit score requirements are a critical consideration for anyone seeking homeownership. If you're planning to purchase a home or refinance your current mortgage, understanding the credit score requirements can significantly impact your financial journey. FHA loans, backed by the Federal Housing Administration, are designed to make homeownership more accessible to borrowers who may not qualify for conventional loans.

Chase Bank, one of the leading financial institutions in the United States, offers FHA loans to help borrowers secure competitive rates and favorable terms. However, meeting the credit score requirements is essential to ensure approval and access to the best loan options. In this guide, we will explore everything you need to know about Chase FHA loans and their credit score criteria.

This article is crafted to provide actionable insights and expert advice to help you navigate the process of securing an FHA loan through Chase. Whether you're a first-time homebuyer or a seasoned borrower, this guide will equip you with the knowledge to make informed decisions about your mortgage.

Introduction to FHA Loans

FHA loans have become a popular choice for borrowers looking to purchase homes with lower down payments and flexible credit requirements. These loans are insured by the Federal Housing Administration, making them an attractive option for first-time buyers and individuals with less-than-perfect credit histories.

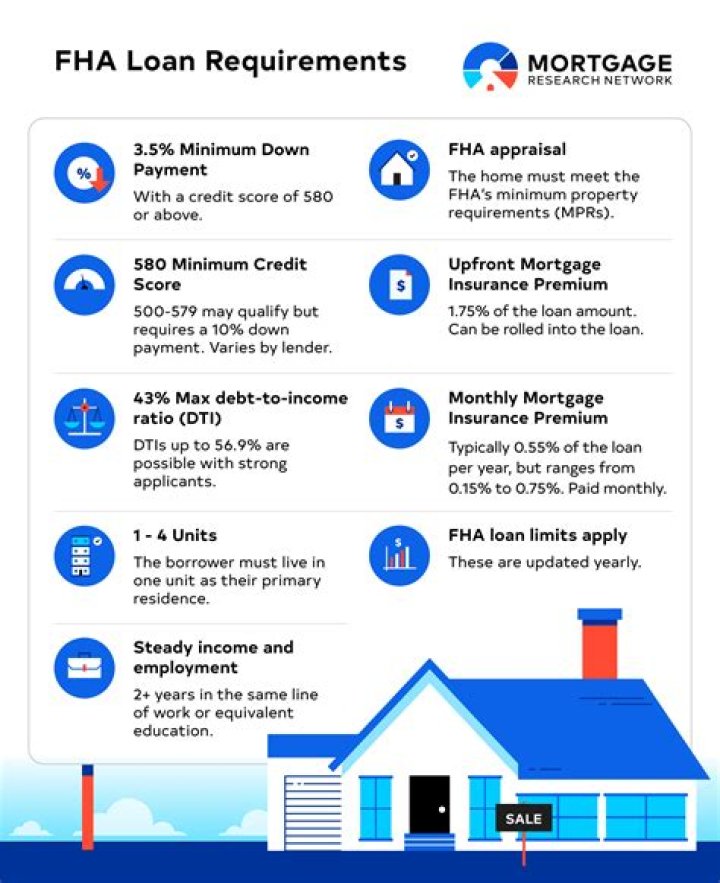

One of the primary advantages of FHA loans is their accessibility. Borrowers with credit scores as low as 500 may qualify, although a score of 580 or higher is typically required to secure the minimum down payment of 3.5%. This flexibility makes FHA loans an excellent option for those who might otherwise struggle to obtain financing.

Why Choose an FHA Loan?

FHA loans offer several benefits, including:

- Lower down payment requirements

- Flexible credit score criteria

- Access to competitive interest rates

- Options for both home purchases and refinancing

Chase FHA Loan Basics

Chase Bank is a trusted lender offering FHA loans to borrowers across the United States. As one of the largest financial institutions, Chase provides a range of mortgage options, including FHA loans, tailored to meet the needs of diverse borrowers.

When applying for a Chase FHA loan, borrowers can expect a streamlined process with dedicated support from experienced loan officers. Chase also offers online tools and resources to simplify the application process and provide transparency throughout the journey.

Key Features of Chase FHA Loans

- Competitive interest rates

- Flexible credit score requirements

- Low down payment options

- Access to mortgage insurance premium (MIP) reductions

Credit Score Requirements for Chase FHA Loans

Understanding the credit score requirements for Chase FHA loans is crucial for borrowers seeking approval. While FHA loans are known for their lenient credit criteria, Chase may impose additional guidelines to ensure loan quality and borrower stability.

As of the latest updates, borrowers generally need a credit score of at least 580 to qualify for the minimum 3.5% down payment. Scores below 580 may still qualify, but a higher down payment is typically required. Chase may also evaluate additional factors, such as debt-to-income ratio and employment history, to determine eligibility.

Factors Influencing Credit Score Requirements

- Loan-to-value ratio

- Debt-to-income ratio

- Employment stability

- Credit history

FHA Loan Eligibility Criteria

Eligibility for Chase FHA loans extends beyond credit score requirements. Borrowers must meet specific criteria to qualify, including residency status, income verification, and property eligibility.

One key requirement is that the property being purchased must be the borrower's primary residence. Investment properties and vacation homes are not eligible for FHA financing. Additionally, borrowers must meet citizenship or legal residency requirements.

Eligibility Checklist

- Primary residence requirement

- U.S. citizenship or legal residency

- Stable employment history

- Sufficient income for loan repayment

Down Payment and Other Costs

One of the most appealing aspects of FHA loans is the low down payment requirement. Borrowers with a credit score of 580 or higher can secure a loan with as little as 3.5% down. However, it's important to note that FHA loans require mortgage insurance premiums (MIP), which add to the overall cost of the loan.

MIP is typically paid upfront and annually throughout the life of the loan. Borrowers may also incur closing costs, which can range from 3% to 5% of the loan amount. Chase offers options to finance closing costs into the loan, making the initial out-of-pocket expenses more manageable.

Breaking Down FHA Loan Costs

- Down payment: 3.5% of the loan amount

- Mortgage insurance premium (MIP)

- Closing costs: 3%-5% of the loan amount

Benefits of FHA Loans

FHA loans offer numerous benefits that make them an attractive option for borrowers. From flexible credit requirements to competitive interest rates, these loans provide a pathway to homeownership for many individuals who might otherwise struggle to qualify.

Some of the key advantages include:

- Lower down payment requirements

- Flexible credit score criteria

- Access to competitive interest rates

- Options for both home purchases and refinancing

Why Choose Chase for Your FHA Loan?

Chase Bank stands out as a trusted lender offering FHA loans with competitive terms and exceptional customer service. Borrowers can expect a seamless application process, transparent communication, and access to a wide range of resources to support their homeownership journey.

Common Questions About FHA Loans

Many borrowers have questions about FHA loans and their eligibility. Below are some of the most frequently asked questions and their answers:

Q: Can I use an FHA loan for a second home?

A: No, FHA loans are only available for primary residences. Investment properties and vacation homes are not eligible for FHA financing.

Q: What happens if my credit score is below 580?

A: Borrowers with credit scores below 580 may still qualify for an FHA loan, but a higher down payment is typically required.

Q: Can I refinance an existing mortgage with an FHA loan?

A: Yes, FHA loans can be used for both home purchases and refinancing. The FHA Streamline Refinance program offers simplified options for borrowers looking to reduce their monthly payments.

How to Improve Your Credit Score

Improving your credit score can increase your chances of qualifying for a Chase FHA loan with favorable terms. Here are some strategies to boost your credit score:

- Pay bills on time

- Reduce outstanding debt

- Limit new credit inquiries

- Monitor your credit report for errors

By implementing these strategies, you can enhance your creditworthiness and improve your eligibility for an FHA loan.

Steps to Apply for a Chase FHA Loan

Applying for a Chase FHA loan involves several steps, from gathering necessary documentation to completing the application process. Here's a step-by-step guide to help you navigate the journey:

Step 1: Gather Required Documentation

Prepare the following documents:

- Proof of income (pay stubs, W-2 forms)

- Tax returns for the past two years

- Bank statements

- Employment verification

Step 2: Pre-Approval Process

Complete the pre-approval process to determine your borrowing capacity and lock in a competitive interest rate.

Step 3: Submit Your Application

Submit your application through Chase's online platform or with the assistance of a dedicated loan officer.

Conclusion and Next Steps

Chase FHA loan credit score requirements are designed to make homeownership accessible to a broad range of borrowers. By understanding the eligibility criteria, costs, and benefits of FHA loans, you can make informed decisions about your mortgage options.

We encourage you to take the next step by gathering your documentation and reaching out to Chase for pre-approval. Additionally, consider improving your credit score to increase your chances of securing favorable terms.

Feel free to leave a comment or share this article with others who may benefit from the information. For further guidance, explore our other resources on homeownership and mortgage financing.

References: