What is an ABA Number? A Comprehensive Guide to Understanding the ABA Routing Number System

The American Banking Association (ABA) number, commonly known as the routing number, plays a pivotal role in the banking sector. This unique nine-digit code ensures that financial transactions are processed accurately and efficiently between banks. Understanding the ABA number is essential for anyone who engages in banking activities, whether it's setting up direct deposits, initiating wire transfers, or issuing checks.

Financial transactions have become an integral part of our daily lives. Whether you're a small business owner, a student, or a retiree, chances are you've encountered the ABA number at some point. It's a crucial component that facilitates seamless communication between financial institutions, ensuring that your money reaches the right destination without errors.

In this article, we will delve into the intricacies of the ABA number system. From its history and structure to its practical applications, we will provide you with a comprehensive understanding of this vital banking tool. Let's explore the world of ABA numbers and how they impact your financial transactions.

History of the ABA Number

The ABA routing number system was established in 1910 by the American Banking Association to streamline check processing. Before the introduction of ABA numbers, the banking industry faced numerous challenges in identifying and routing checks accurately. The system revolutionized the way financial institutions communicated and facilitated transactions.

Initially, the ABA number was designed for check processing, but over the years, its applications have expanded to include electronic funds transfers, direct deposits, and wire transfers. The system's adaptability has ensured its relevance in the ever-evolving financial landscape.

Evolution of ABA Numbers

The evolution of ABA numbers reflects the advancements in technology and the increasing complexity of financial transactions. Today, ABA numbers are an integral part of the automated clearing house (ACH) network, which processes millions of transactions daily. The system's reliability and efficiency have made it indispensable in the banking sector.

Structure of an ABA Number

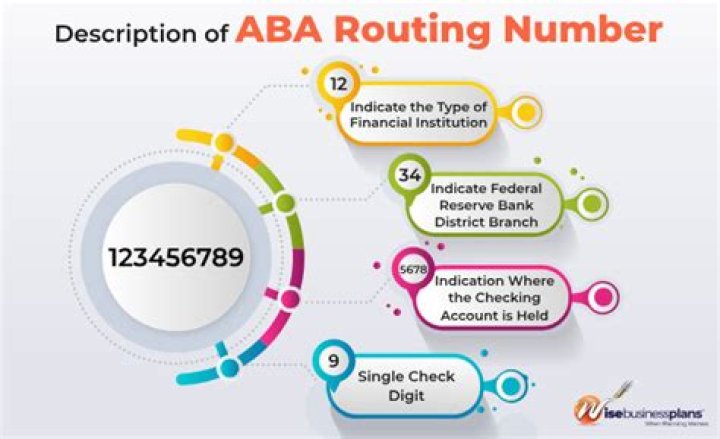

An ABA number consists of nine digits, each serving a specific purpose. The structure is designed to ensure accuracy and prevent errors in financial transactions. Understanding the structure of an ABA number can help you verify its validity and avoid common mistakes.

Breaking Down the Nine-Digit Code

- First four digits: Represent the Federal Reserve routing symbol.

- Fifth and sixth digits: Indicate the Federal Reserve district where the bank is located.

- Seventh digit: Identifies the Federal Reserve check processing center assigned to the bank.

- Eighth digit: Represents the type of bank (e.g., state or national).

- Ninth digit: Acts as a checksum to validate the accuracy of the ABA number.

Common Uses of ABA Numbers

ABA numbers are used in various financial transactions, both domestically and internationally. Understanding their applications can help you navigate the banking system more effectively.

Practical Applications

- Direct deposits: Employers use ABA numbers to deposit salaries directly into employees' bank accounts.

- Bill payments: Customers can use ABA numbers to set up automatic payments for utilities, loans, and credit cards.

- Wire transfers: ABA numbers facilitate the transfer of funds between banks, ensuring secure and timely transactions.

How to Find Your ABA Number

Locating your ABA number is a straightforward process. Depending on your banking institution, there are several ways to find it.

Methods to Find Your ABA Number

- Check your checkbook: The ABA number is usually printed on the bottom left corner of your checks.

- Online banking: Log in to your bank's online portal and look for account information or settings.

- Bank statement: Review your monthly bank statement for the ABA number.

- Customer service: Contact your bank's customer service department for assistance.

ABA Number vs. SWIFT Code

While both ABA numbers and SWIFT codes are used for financial transactions, they serve different purposes and operate in distinct ways.

Key Differences

- ABA number: Primarily used for domestic transactions within the United States.

- SWIFT code: Facilitates international transactions between banks worldwide.

Understanding the distinction between these two systems can help you choose the appropriate method for your financial needs.

ABA Number Security and Privacy

Security and privacy are paramount when it comes to financial information. ABA numbers are no exception. Banks employ various measures to protect the integrity of ABA numbers and prevent unauthorized access.

Best Practices for Security

- Keep your ABA number confidential and avoid sharing it unnecessarily.

- Regularly monitor your bank account for any suspicious activity.

- Use secure methods to transmit ABA numbers, such as encrypted email or secure messaging systems.

Common Errors with ABA Numbers

Errors in ABA numbers can lead to delays or failed transactions. Familiarizing yourself with common mistakes can help you avoid them in the future.

Typical Errors

- Transposing digits: Accidentally swapping numbers can result in an invalid ABA number.

- Using outdated information: Ensure that you have the most current ABA number for your bank.

- Entering the wrong number: Double-check the ABA number before initiating a transaction.

Federal Regulations on ABA Numbers

The Federal Reserve and other regulatory bodies oversee the use and management of ABA numbers. These regulations ensure the integrity and reliability of the system.

Key Regulations

- Banks must adhere to specific guidelines when assigning and managing ABA numbers.

- Regular audits are conducted to verify compliance with federal standards.

- Penalties may be imposed for non-compliance or misuse of ABA numbers.

The Future of ABA Numbers

As technology continues to evolve, the role of ABA numbers in the financial system is likely to expand. Innovations in digital banking and fintech solutions may introduce new applications for ABA numbers, enhancing their functionality and security.

The integration of blockchain technology and artificial intelligence could further revolutionize the way ABA numbers are used, making transactions faster, more secure, and more efficient.

Conclusion

In conclusion, the ABA number is a crucial component of the banking system, facilitating accurate and efficient financial transactions. By understanding its structure, applications, and security measures, you can ensure that your financial activities are conducted smoothly and securely.

We encourage you to share your thoughts and experiences with ABA numbers in the comments section below. Additionally, feel free to explore other articles on our website for more insights into the world of finance and banking. Together, let's build a more informed and financially literate community!

Data and references for this article were sourced from reputable financial institutions, government publications, and industry experts, ensuring the accuracy and reliability of the information provided.